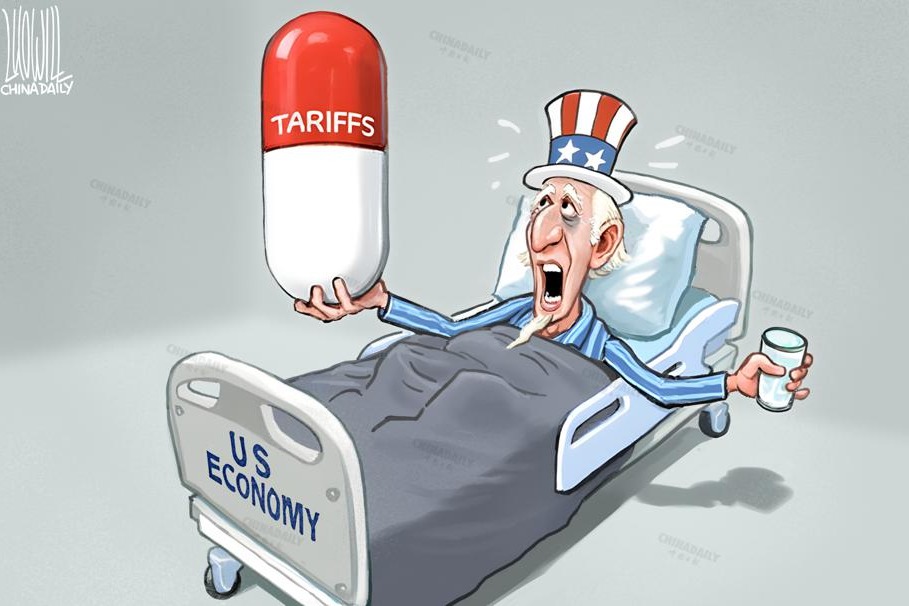

US no longer plays by monetary rules

Editor's note: The US Federal Reserve's interest rate hikes have negative spillover effects on the global economy, with its monetary policy decisions having a significant impact on the global stock market. But the US, given the dollar's dominance of the international monetary system, cares least about the global economy. Four experts share their views on the issue.

In The Economic Weapon: The Rise of Sanctions as a Tool of Modern War, historian Nicholas Mulder reminds us that even when Britain and Russia were savagely battling each other during the 1853-56 Crimean War, they continued to service their debts to each other. Likewise, when hedge funds launched predatory attacks on Asian currencies during the 1990s Asian financial crisis, they still played by the rules (even though their unethical behavior brought some East Asian economies' progress to a halt).

The United States' Feb 28 decision to freeze about half of Russia's foreign exchange reserves would seem to fall into a different category. Although the US has taken similar actions against Iran, Venezuela and Afghanistan, Chinese economists thought those were exceptional situations, and find it shocking that the US would carry out such measures against Russia.

The international financial system is based on the trust that all participants will play by the rules, and honoring debt obligations is one of the most important rules there is. Whatever the justification, freezing a country's foreign exchange reserves is a blatant breach of that trust. The US, which issues the main global reserve currency, is jeopardizing its financial credibility for the sake of some elusive short-term tactical advantages. That is a big mistake.

For many years, China's ability to amass foreign exchange reserves was a symbol of its burgeoning economic success. But it has been a controversial issue since the mid-1990s (when China's reserves reached $100 billion), because the purpose of trade is not to earn ever-greater foreign exchange reserves, but rather to participate in the international division of labor in a way that improves resource allocation across borders.

The Asian financial crisis in 1997 seemed to vindicate the argument that China needed large foreign exchange reserves with which to fend off predatory attacks by international speculators. By 2003, China's reserves had quadrupled to $400 billion, and there was growing international pressure on Chinese authorities to allow the renminbi to appreciate. But they were reluctant to do so, because they didn't want to cause a slowdown in export growth. China's vast foreign exchange holdings thus continued to increase at an accelerated pace.

Then came the 2008 global financial crisis, which compelled China to recognize that its foreign exchange reserves might be in jeopardy. Wen Jiabao, then Chinese premier, expressed these concerns publicly in March 2009: "We have lent a huge amount of money to the US, so of course we are concerned about the safety of our assets. Frankly speaking, I do have some worries." He then urged the US government to "maintain its credibility, honor its commitments, and guarantee the security of Chinese assets".

The US government did honor its commitments, and China carried on accumulating foreign exchange reserves, which peaked at $3.8 trillion in 2014, before falling by $800 billion in the following two years as China's central bank intervened heavily in the foreign exchange market to stabilize the renminbi in the face of large capital outflows. Since 2016, China's reserves have been around $3 trillion under a more flexible exchange rate regime, even though it has continued to run a current account surplus. Today, they stand at around $3.2 trillion.

But there are two big reasons why it should reduce the reserves. First, with more than $2 trillion of net international assets, China's net investment income has been negative for almost 20 years, because its holdings are disproportionately in low-yield US Treasuries. This is a grotesque misallocation of resources.

Second, the US dollar eventually may fall significantly, because the US has been running huge net foreign and national debts for decades, and this shows no signs of changing. Moreover, the US Federal Reserve's expansionary monetary policy (in the form of quantitative easing) may continue to create inflationary pressure in the future.

To be sure, with many countries, especially China, holding such large amounts of dollar-denominated foreign exchange reserves, the US dollar can remain strong for quite some time. But at some point, the greenback's value will fall, and the second-largest foreign holder of US Treasuries-China-will face huge losses.

Given this possibility, I have long advocated a floating exchange rate regime for the renminbi; a cautious approach toward capital-account liberalization; diversification of foreign-exchange reserves; patient, market-driven internationalization of the renminbi; and more balanced trade with the US. But all these suggestions assume that the US will play by the rules.

Now that the US has unilaterally frozen the Russian central bank's foreign exchange reserves, the foundation for my policy recommendations has crumbled.

If all foreign assets, public as well as private, can be frozen in a split second by reserve-currency countries, policymakers should not even waste their time with hedging measures like diversification. And since the US has stopped playing by the rules, what can China do to safeguard its foreign assets? I don't know. But I am sure that Chinese policymakers, and perhaps those in other countries as well, will be thinking very hard about solutions.

Project Syndicate

The author, a former president of the China Society of World Economics and director of the Institute of World Economics and Politics at the Chinese Academy of Social Sciences, served on the Monetary Policy Committee of the People's Bank of China from 2004 to 2006. The views don't necessarily reflect those of China Daily.

If you have a specific expertise, or would like to share your thought about our stories, then send us your writings at [email protected], and [email protected].